The possibility of multiple branches within the company and multiple companies within the group

The possibility of doing a financial position at the branch level and at the company level. This position will be multi-financial years and multiple financial periods with the ability to close any financial period (preventing entry, modification or cancellation)

It allows the user to distribute expenses and revenues on the branches and cost centers in addition to the possibility of distributing also among three additional dimensions (such as project - item - .... etc.)

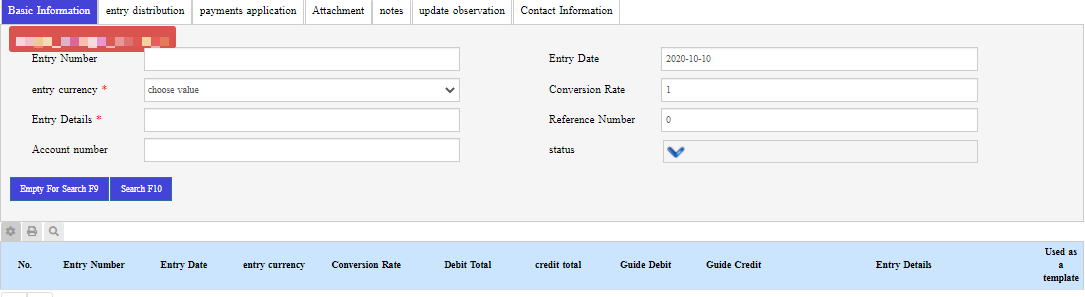

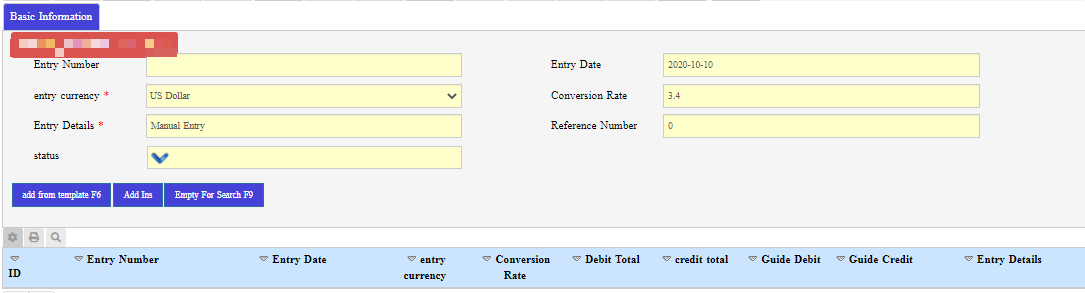

The possibility of numbering the daily entries automatically or manually

Integration between public accounts and the rest of the systems so that the user can see the entries sent from each system

The possibility of defining the accounting periods, as there is a variable in the definition of establishments that clear the accounting periods that the establishment follows. accordingly, the fiscal year is distributed over these periods

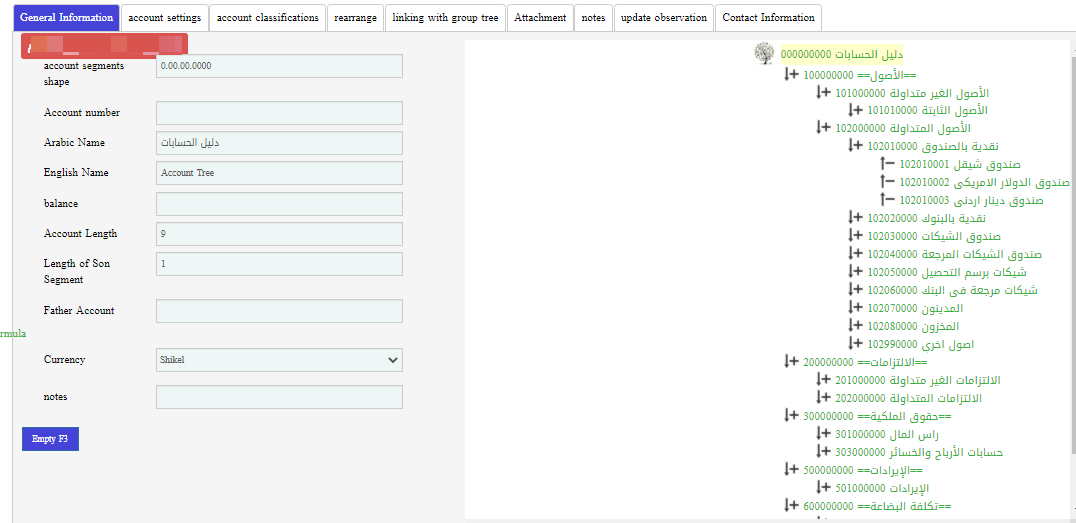

The ability to define a directory of accounts with a fixed length for the account number

The possibility of determining the currency of the directory when it is created, as well as determining the length of the account to be created

The ability to add the account currency to the account

The possibility of dividing the accounting entries into 3 stages

The first stage (which is not included in the accounting operations) where the entry is not considered an entry until it is saved as an entry

The second stage: the entries that not carried over, which are the entries that have been saved, but there will be a review process on it, and in the review it is possible to make amendment on the entry data

The third stage: the carried over entries: the entries that cannot be modified. The ledger account: where any account can be known whether it is a credit or debit (knowing the account balance)

carry over (Posting) the entries to the journal, where each department has an assistant ledger

The possibility of creating balance sheet at any time without the need to close the accounting periods and on more than one level according to the accounting guide

creating balance sheets.

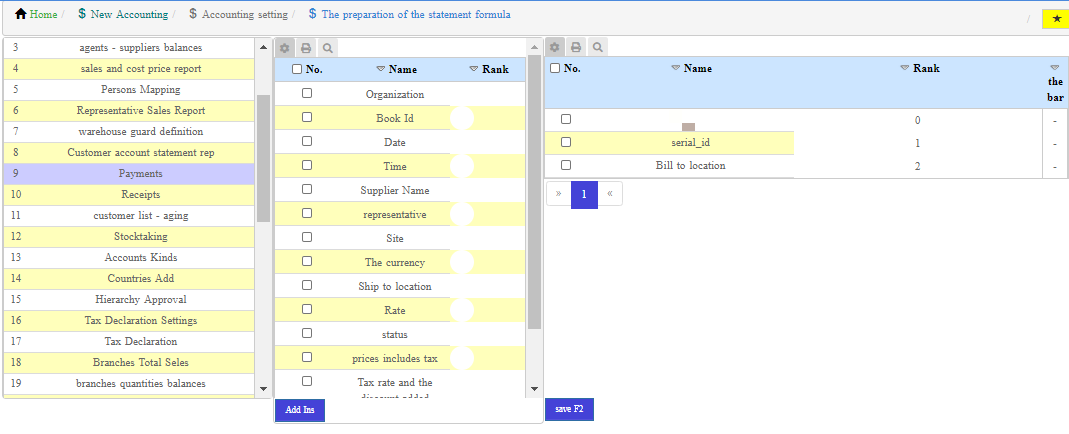

Preparing the statement format

The format of the statement is prepared for the operations inside the system according to the desire of the establishment, so what is shown in the statement is chosen and choose the order of the breaks between

Statement criteria

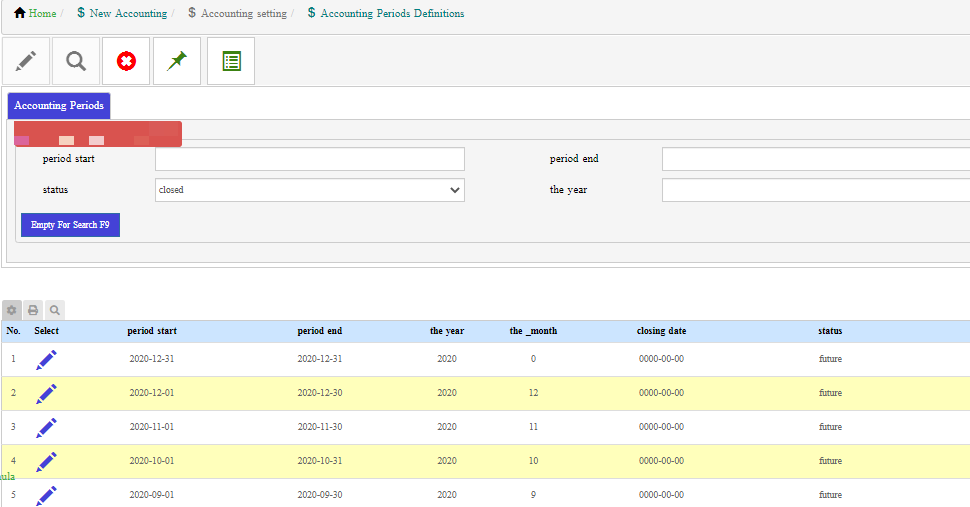

Definition of accounting periods

Accounting periods are defined based on their definition in "establishments management" when defining the establishment, so that they contain three cases for each accounting period and they are:

a future period, an open period, and a closed period

As transactions are added and posted in the future and open periods, and the system prevents us from posting to a closed period until it is reopened to be posted again. There is also an independent period called the "settlement period" and it will be at the end of the financial period, and it concerns the settlement and closing entries of the establishment

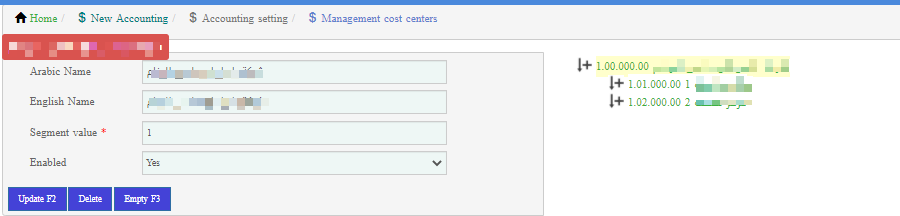

Cost centers management

In cost center management, the required cost centers are added to the organization, and the cost centers are added based on the pre-set up of a structure the length of the section for the cost center shape in "organization management settings" where cost centers are added in a hierarchical shape as in the chart of the accounts

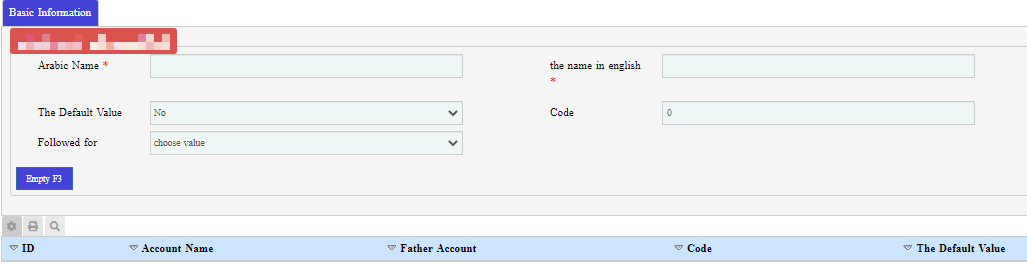

Sub-accounts

Through the sub-accounts, the sub-accounts of the establishment are added, which are additional information that is added to financial transactions

by adding them in the system. For example: when entering a bill of exchange for fuels, it is possible to specify these fuels belonging to a specific car, in case that there are several cars for representative., and this information is used later in the reports

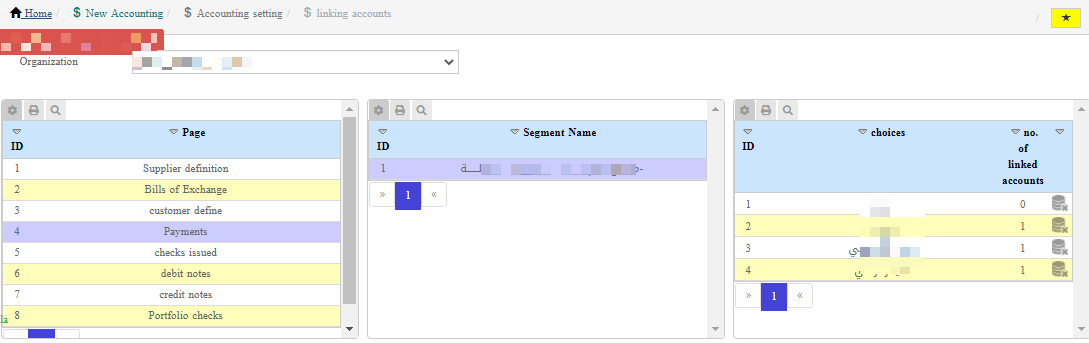

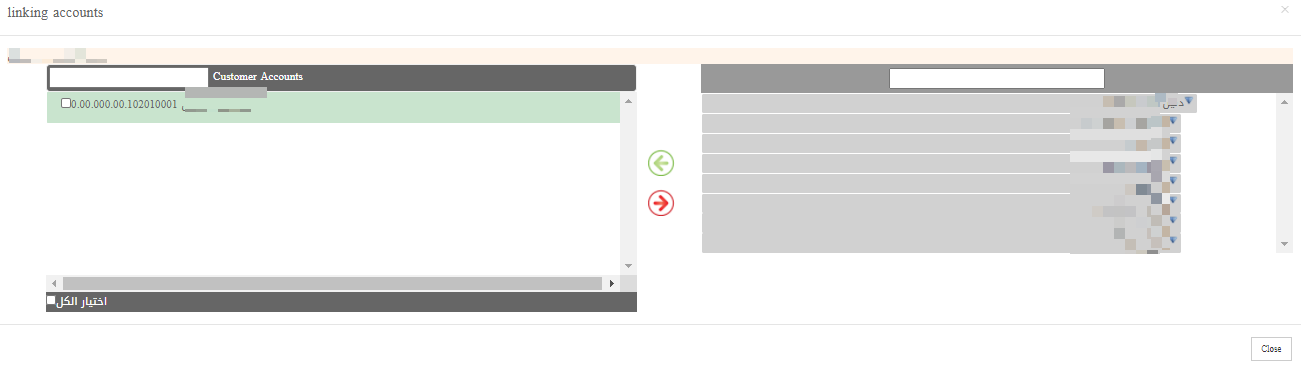

Linking accounts

Linking the accounts after preparing the accounts sections and giving them to the users, after that the account sections are linked to the accounts in the accounts directory to be used in the accounting entries resulting from financial transactions from the windows of the system

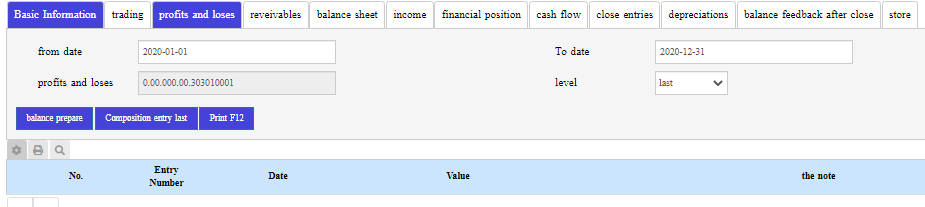

Preparing the financial statements

The financial statements of the establishment are prepared where the result of the establishment’s business is presented through several reports, including: trading account, profit & loss account, balance sheet, income statement, list of financial position, accounts Receivable Balances, cash flow statement, closing entry the financial year of the establishment, list of depreciation of fixed assets, and finally, the trial balance is displayed after the close of the financial year of the establishment

The system also provides the user with a mechanism to prepare financial statements at the levels of the chart of accounts to reduce the volume of data presented for analysis financial statements according to a comprehensive view of the corporation

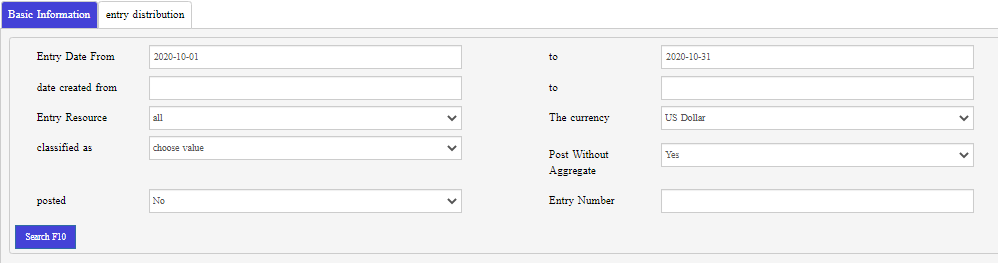

Journal posting settings

Through the journal posting settings, accounting entries will be automatically posted from the journal to GL-Posting according to a specific period of time, such as: 5 days

Settings for automatic posting

Through the automatic posting settings, the accounting entries will be automatically posted from the GL-Posting window to the posted accounting entries window. In addition to the ability to collect entries before posted according to a specific time period in minutes, such as: a posting every 30 minutes

Credit Card Settings

Through the credit card settings, the names of the banks and subsidiary banks related to each major bank are listed, as well as the sub-bank account numbers

and the internal account numbers in the organization that were defined in the accounts guide to use these settings when dealing with the credit card in financial transactions, such as: sales

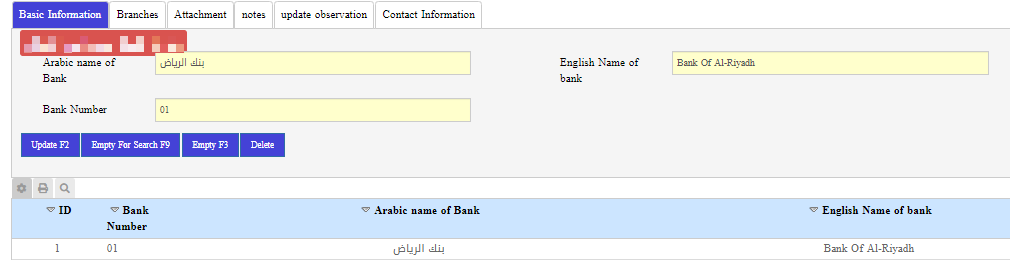

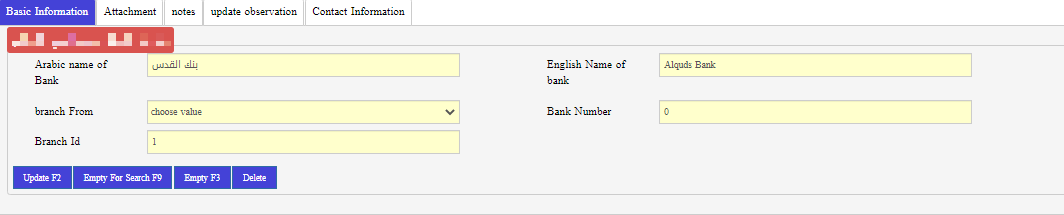

Banks

Through the banking window, all the banks that will be dealt with in financial transactions are listed, as they will be used in the outgoing & incoming cheques later

General Ledger

Posting General Ledger entries, it is a window in which all accounting entries are collected from all accounting operations in the journal and the daily entries from the system, then they are posted to the last two stages, which are: the accounting entries window that is not posted (before the final posting) or the accounting entries window posted posting (final posting). Where the latter is based on which the financial statements of the corporation are prepared

Posted account entries

It is the final stage of the accounting entries cycle, as the financial statements are created based on the accounting entries carried out which comes from the "GL-Posting" window, and the accounting entries are in the currency of the system, but to know the accounting entry in its currency, the entry or revision of the entry is done through the "GL-Posting Posting Entries" window

Non-posting accounting entries

It is a temporary stage for the accounting records cycle, where the entries are collected for a specific reason in the organization and then the entries are posted from it to the posted accounting window. The posted accounting at this stage are not included in the financial statements. And also its source is GL-Posting Entries window And the accounting entries are in the system currency, but to know the accounting entry in its entered currency or revision

The entry is through the "GL-Posting" window

Adding / modifying manual entries

Through the window of adding / modifying entries, manual accounting entries are entered into the system, where the basic information for the entry is entered and then the registration details are entered from the other window

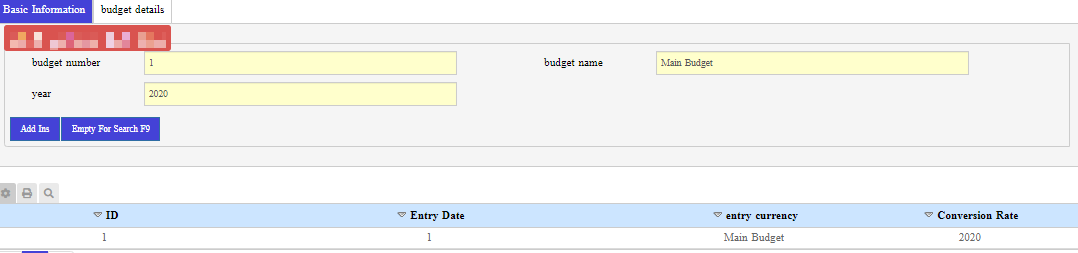

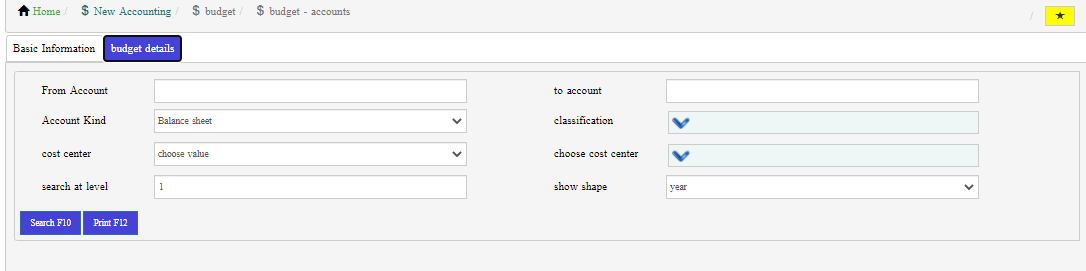

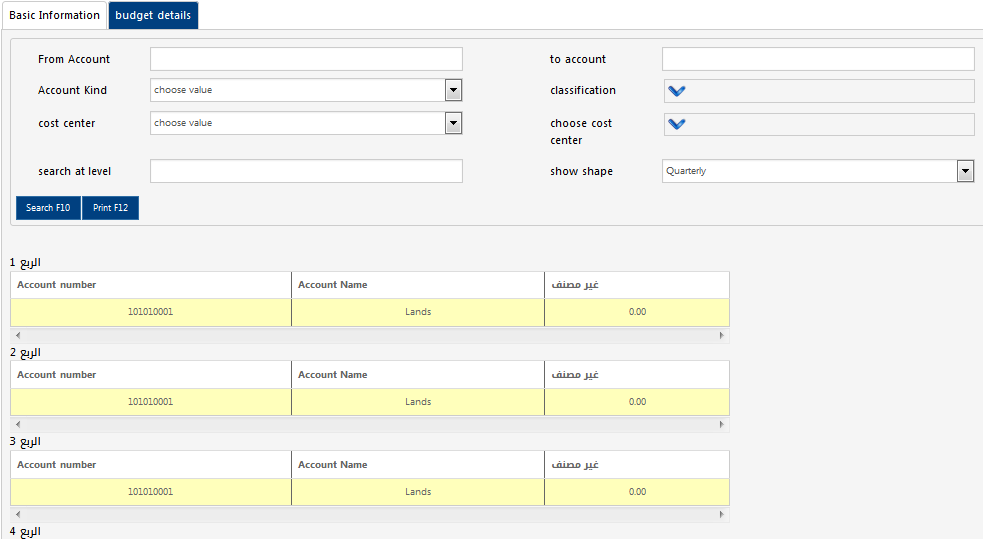

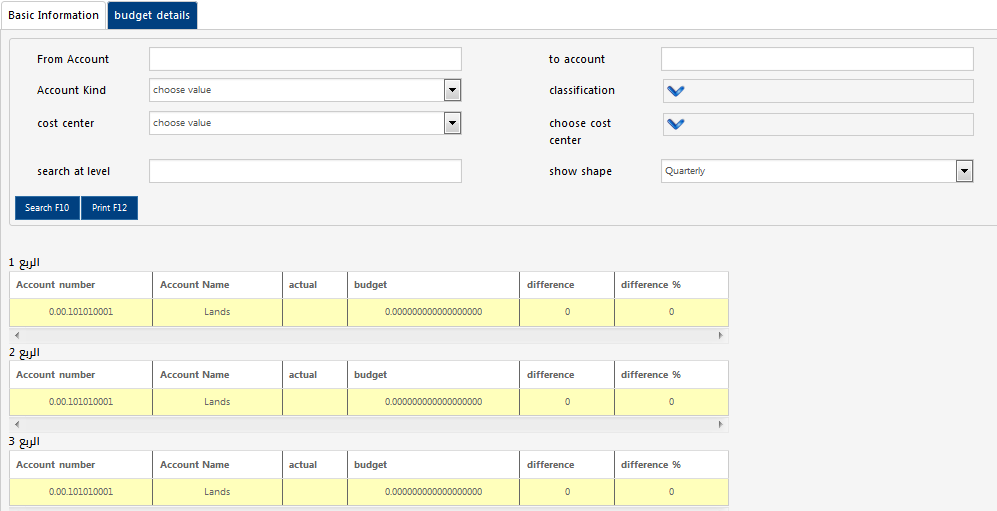

Budgets

The budget is a financial translation of a quantitative plan that covers all aspects of the project's activities for a future period in a comprehensive and coordinated form.

The executing officials are linked to it and it takes aa a goal on the basis of following the actual implementation and monitored the results , and it enables the management to take

Corrected procedures to treat the deviations and reach maximum efficiency.

The basic purpose of the budget is to convert the overall strategy of the organization into action, and it is a detailed plan to achieve short and long-term organization objectives, The successful budget does not control the costs only, but also works to ensure that the daily operations are running properly to achieve the company's future goals

Budget objectives

The budget’s objective can be identified by stating its role in the areas of planning and control, as planning and control have become an essential work for any

Contemporary scientific administration that wants to achieve its goals as efficiently and effectively as possible

Planning tries to study how to achieve goals through a coordinate set of planned processes, while control tries to conform with the processes of achieving goals by implementing the set plans

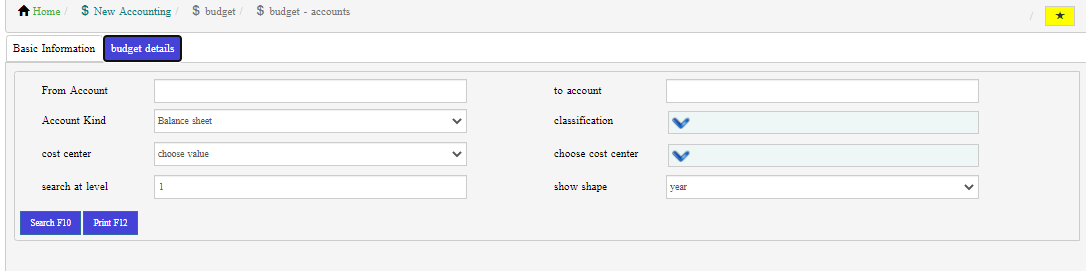

Budget preparation

The system is characterized by the availability of budgets on the basis of accounts and also on the basis of cost centers, as well as the ability to compare actual use and the expected use to show the difference between them in the organization reporting and analysis, where the accounts are inserted and for any dependent cost center, if any, and then the required accounts are established, then the monthly amounts are entered for each account. Also can make a budget for the following matters